DCS’s design and engineering team has more than 40 years of experience creating unique parcel handling systems for diverse customer applications. With installations including semi-automated handling in small city distribution centers and fully automated, integrated hubs with advanced conveyor and sorter equipment, DCS routinely thinks outside the box.

DCS designs and implements end-to-end warehouse automation solutions for e-commerce and multi-channel retailers that address numerous workflow challenges. This includes solutions for receiving, putaway, storage, replenishment, order fulfillment, picking, packing, sortation, and outbound shipping. Our custom integrated warehouse, distribution, and fulfillment systems draw from a deep pool of conventional, semi-automated, and automated material handling technologies.

Whether an operation is considering the construction of a new distribution or fulfillment center, or a retrofit or expansion of an existing facility, it’s important to create a solution that fits the overarching supply chain strategy. DCS has four decades of experience designing and integrating comprehensive, end-to-end material handling solutions that meet a multitude of operational goals. Whether conventional, semi-automated, or fully automated, DCS can help your organization implement a custom solution that meets its goals while maximizing return on investment (ROI).

The DCS Supply Chain Consulting team offers a range of services to help your operations address the challenges it faces. Working in partnership with you, DCS consultants analyze your business data- existing workforce, workflow processes, inventory, order data, operations, and more- to determine a strategy that addresses your unique needs. Whether you need an operations assessment, process improvement recommendations, or distribution design services, DCS consultants will help guide you to the material handling system or operational solution that best meets your current and future needs, as well as your budget.

Keeping your warehouse operations and material handling systems running smoothly and at the peak of productivity are the goals of DCS’ Customer Service Team. By partnering with DCS, your warehouse automation solution is supported from commissioning to end of life. You’ll receive comprehensive in-house training of your personnel, including specialized training of your designated internal system expert. Plus, DCS offers a complete package of spare parts and expert system troubleshooting support from qualified engineers dedicated to your installation.

DCS offers a broad range of material handling equipment and automated system design, installation, and integration services for a multitude of projects. These include retrofits, expansions, upgrades, and more. While every project is unique, our system design and execution processes are the same, encompassing meticulous attention to detail, frequent communication, and a dedicated partnership with our clients.

Designed Conveyor Systems (DCS) has 40 years of experience serving major clients in multiple industries by providing material handling, full-scale warehouse operations, and conveyor design solutions that are custom crafted for their needs. DCS does not sell ready-made conveyor systems but builds relationships that empower collaboration to craft custom warehouse designs together. DCS utilizes consulting, engineering design, project management, installation services, and client support to ensure our customers can keep their promises to deliver on time.

With more than 40 years of experience providing automated system design, installation, and integration services, DCS has created solutions for companies throughout the United States in a broad range of industries and markets. We’ve completed more than 1500 projects ranging from greenfield facilities with completely new systems to expansions and retrofits of existing operations.

Designed Conveyor Systems values building strong relationships with our clients. Join us at our upcoming events to collaborate and discover how we can design a custom warehouse solution tailored to your unique needs.

By submitting, you consent to DCS processing your information in accordance with our Privacy Policy. We take your privacy seriously; opt out of email updates at any time.

This site is protected by reCAPTCHA and the Google Privacy Policy and Terms of Service apply.

Annually, Modern Materials Handling and Logistics Management magazines team up with Peerless Research Group to produce an Industry Outlook study and report. The publications’ goal is to gain a better understanding of current market conditions, trends, and best practices in manufacturing, warehousing, and distribution operations.

The last report was released January 2021. Now that we’re starting a new year, I took a look back at their findings as I was reflecting on the past 12 months to compare with what we actually witnessed in the material handling industry. Overall, the report got the general trends correct, but the growth we’ve seen has surpassed the original expectations. This isn’t surprising when you consider the magnitude of the marketplace changes that happened over the past 18 months. COVID caused a 10-year leap in e-commerce adoption in a short time period, and the infrastructure is playing catch-up.

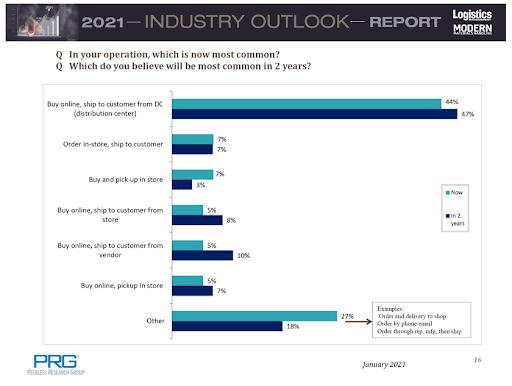

Indeed, when asked what type of order fulfillment was most prevalent among respondents to the survey, 44% said Buy online, ship to customer from distribution center (DC) as seen in Figure 1 below. In another two years, survey participants expected growth to 47%. Last year, we saw new industrial leases dedicated to e-commerce operations drastically outpace other segments’ growth, and now those spaces need to be outfitted to support the operations.

This exponential uptick in demand for direct-to-consumer shipments has overwhelmed retailers. While many operations have some type of material handling equipment and technologies in place, many of those systems are purpose-built for a different type of handling (larger orders, retail store replenishment, etc.). That is, facilities have systems that are not optimized to meet the handling demands that come with shipping smaller orders-driven by both B2C and B2B changes in expectations. To successfully shift from shipping full or mixed case pallet loads for retail store replenishment to picking, packing, and shipping each requires a totally different type of equipment-in many cases, it calls for some degree of automation.

Recognizing that, more operations reported attempting to pivot their operation by purchasing and implementing material handling equipment and software that allows them to fulfill a vastly different order profile than what they historically handled. That definitely occurred in 2021. Interestingly, according to the survey, more companies said they planned to proceed with investments in material handling equipment, regardless of the economy, in 2020 (63%) than they expected to in 2021 (56%) when the majority expected to take a more conservative approach, as seen in Figure 2.

However, upon closer inspection, the makeup of the continue to spend group aligns with the e-commerce jump. Automatic guided vehicles (AGVs) and robotics (both often associated with manufacturing and larger order movements such as pallets) dropped off for 2021, but conveyors, sortation, and software-which are the stalwarts of e-commerce operations-all increased. One noticeable omission from the list is autonomous mobile robot (AMR) technology (vastly different applications from AGVs), which could see increased adoption in the e-commerce fulfillment arena in the near future.

Many organizations already know what the ultimate objective is for the solutions they implement: faster fulfillment. To reach that goal companies are prioritizing four key practices in their operations today (and even more so in the future), as seen in Figure 3:

Continuous improvement (Now 64%; In two years 72%)

Labor productivity measurement/management (Now 61%; In two years 68%)

Workload planning (Now 53%; In two years 66%)

Same-day order shipping (Now 51%; In two years 58%)

This correlates with what my colleagues and I have been seeing in the last 24 months. In fact, I suspect the continuous improvement category actually is the foundation of the other three practices-as in, companies recognize that they need to get better at measuring and managing labor productivity, workload planning, and shipping orders out on the same day they were received.

Additionally, companies acknowledge that issues such as supporting company growth and mitigating the lack of labor availability are critical reasons for investing in their material handling and order fulfillment capabilities. As seen in Figure 4, these two issues are barely eclipsed by safety at the top of the priorities list. These three are most often cited by the organizations we work with and are likely to continue to be so. Many companies are addressing these initiatives with automation-both on the software and hardware fronts.

The report’s respondents also said their companies are pulling out the checkbook, so to speak. In Figure 5, 52% of respondents planned to purchase new equipment or upgrade existing equipment in 2021. The same percentage also planned to invest in more information technology hardware and software during the same timeframe, with the average budget landing at just a hair under $307,000.

These infrastructure costs directly coincide with the increases in automation to support fundamental shifts in businesses. While many have closed or scaled down their brick-and-mortar operations while looking to capitalize on growing small-order fulfillment, we will likely see a phased adoption of certain automation technologies over the next several years.

Looking back at Figure 2, perhaps the 56% of companies that decided to put their material handling investments in a holding pattern recognize that one-size does not fit all when it comes to selecting equipment to handle e-commerce order fulfillment. After all, the categories of new equipment and information technology hardware and software cover a lot of ground.

Is this delay the result of analysis paralysis? Are organizations postponing the spend because they fear purchasing the wrong solution? This probably is indeed the case, when considering the research around the diffusion of innovations and the different types of adopters: innovators, early adopters, early majority, late majority, and laggards. Much like the famous hybrid corn seeds of the Depression-era farmers, automated order fulfillment will be ubiquitous in the near future, and companies will need to decide where on the adoption curve they will be sitting.

Figuring out exactly what e-commerce fulfillment technology solution will meet an operation’s unique goals, issues, and budget in a wildly unpredictable marketplace can truly be daunting. Add to that the pressure of the Amazon effect and consumers’ expectation that whatever they order online could be on their doorstep in as little as four hours, the stakes are high to get the solution right the first time. Yet, while a degree of caution is absolutely critical to ensuring that making a capital expenditure delivers the optimal solution to an operation’s unique challenges, such a delay can put an organization’s very survival at risk. It won’t be long before facilities that are unable to complete same-day order processing will find themselves left behind.

The best approach to achieving the optimal automated e-commerce order fulfillment solution is to work with an equipment supplier and integrator familiar with the industry. That partner should also use a data-centric approach as the basis for selecting the most appropriate technology (or combination of technologies) to address the operation’s specific handling needs. By analyzing a variety of data inputs – such as dimensional and weight information about every stock keeping unit (SKU) stored and handled, the amount of overlap in that data between different SKUs, customer ordering habits, and more – the best-fit material handling equipment and technologies can be optimized for the facility’s unique order profiles.

That said, suppliers of these solutions are not immune to the supply chain shipping and delivery challenges faced by companies worldwide for the past several months. They’re also seeing record demand for their software technologies automated equipment, including conveyors, sorters, goods-to-person systems, robotics, and more. Lead times have only grown longer in the past 18 months. Therefore, it’s become even more important to work with a partner that is brand-agnostic and not affiliated with a specific original equipment manufacturer (OEM). Doing so ensures an organization has access to a wide range of solutions and suppliers in order to source the optimal solution in the best implementation timeframe available.

Need help figuring out how to improve your own fulfillment operations’ outlook?Connect with us.

Matt brings five years of experience in the Material Handling Industry. Matt helps lead a team dedicated to ensuring operations run smoothly for DCS’s partners through maintenance, training, 24/7 support, and life cycle projects. Before entering the Material Handling industry, Matt served eight years as a Naval Officer, filling roles for technical training and ensuring uptime of critical infrastructure on aircraft carriers, including nuclear reactors, electrical distribution systems, and auxiliary engineering equipment. Matt received his Bachelor of Science in Nuclear Engineering and his MBA from The University of Florida. Matt also has PMP and Lean Six Sigma certifications.

Outside of work, Matt enjoys carpentry, running, and open water swimming. He lives in Atlanta, Georgia, with his wife and three kids, where they are trying to raise third-generation competitive swimmers.

")

(1)")